The Strategic Role of Storage in Latin America’s Energy Transition

Regional nations are increasingly embracing the energy transition paradigm, with storage emerging as a critical enabler for wind and solar photovoltaic deployment. Establishing compelling regulatory frameworks remains paramount to this transformation.

Latin America is orchestrating a profound energy transition propelled by the accelerating adoption of renewable energy sources. Analysis from Global Energy Monitor indicates the region has amassed a portfolio exceeding 319 GW of utility-scale solar and wind capacity across various development stages—from permitting to construction—with anticipated commissioning by 2030.

Should these initiatives materialize, the region’s clean energy capacity would experience a remarkable 460% expansion by 2030 compared to 2023 levels, substantially surpassing the current 69 GW threshold (comprising 27.6 GW in solar capacity and 41.5 GW in wind generation). This trajectory would represent an unprecedented 70% expansion beyond the region’s existing aggregate electricity capacity of 457 GW across all generation sources.

Integrating these energy sources yields substantial decarbonization advantages, enabling nations to achieve their climate commitments through fossil fuel displacement and consequent CO₂ emissions reduction.

Additionally, it enhances cost competitiveness. An International Renewable Energy Agency’s (IRENA) analysis published in September of 2024 underscores that wind and solar photovoltaic technologies have achieved superior cost-effectiveness compared to conventional alternatives. Notably, of the 473 GW of new renewable capacity commissioned globally in 2023, an impressive 81% (382 GW) demonstrated greater economic viability than fossil fuel counterparts.

The report further illuminates that global solar photovoltaic costs in 2023 achieved a remarkable 56% cost advantage over fossil fuel and nuclear alternatives.

However, a critical challenge inherent to these clean energy sources lies in their intermittency. Both wind and solar generation operate contingent upon resource availability (wind or sunlight), precluding operators from exercising direct control over supply timing or volume to the grid.

This variability impacts grid stability and precipitates energy curtailment when generation capacity exceeds consumption parameters. The inability to manage energy effectively results in significant resource wastage.

This surplus generation triggers an additional market phenomenon: energy market prices can experience precipitous declines during specific periods. For instance, during peak solar generation hours, combined with wind energy production, prices can deteriorate to $0 per MWh. Conversely, nighttime periods, characterized by substantially reduced supply, can witness sharp price escalations.

Both energy curtailment and price volatility significantly impair the financial performance of enterprises investing in wind and, particularly, solar photovoltaic infrastructure.

To address these challenges, nations globally are increasingly implementing measures to incentivize energy storage—predominantly through battery systems—enabling effective management of variable renewable energy and systematically addressing these operational challenges.

Developments, Project Bankability, and Regulatory Frameworks in Latin America

The “Latin American Energy Storage Summit,” convened October 15–16, 2024, in Santiago, Chile, assembled industry leaders to examine three fundamental pillars of energy storage adoption: technological advancement, project bankability, and regulatory frameworks across Latin American jurisdictions.

These three strategic elements and escalating corporate and governmental engagement across the region underscore storage’s pivotal role in key markets, including Brazil, Chile, Colombia, and Mexico. Renewable deployment is driving substantial growth, with an aggregate capacity exceeding 57 GW.

Advances in Storage

Battery storage has emerged as an optimal complement to wind and solar infrastructure, addressing grid integration challenges. This is particularly true given the dramatic cost reductions in recent years. Between 2010 and 2023, battery project costs have demonstrated an 89% reduction between 2010 and 2023. The International Energy Agency (IEA) projects an additional 40% cost decline between 2023 and 2030.

Installation capacity projections appear equally promising. IEA data indicates that energy sector battery utilization surpassed 2,400 gigawatt-hours (GWh) in 2023, quadrupling 2020 levels. This trajectory is expected to maintain a 25% compound annual growth rate through 2030.

The IEA further projects that global energy storage capacity must increase sixfold by 2030—reaching 1,500 GW—to support the objective of tripling wind and solar installations in support of climate mitigation goals.

Regulation: Clear Frameworks for Storage Development

The regulatory framework is decisive in constraining or accelerating energy storage deployment across jurisdictions.

According to Inter-American Development Bank (IDB) analysis, primary regulatory impediments and challenges inhibiting rapid energy storage adoption in Latin America and the Caribbean encompass:

– Absence of precise energy storage definition within regulatory frameworks: This deficiency constrains the ability to adequately monetize and compensate for the multiple services provided by battery energy storage systems (BESS).

– Suboptimal pricing and tariff mechanisms: This impedes equitable compensation for BESS contributions, as the services provided lack appropriate valuation metrics.

– Insufficient markets for ancillary services in substation management: This restricts potential remuneration and business models available to BESS investors.

– Inadequate incentives for behind-the-meter (BTM) storage installations: This impacts residential, industrial, and commercial self-consumption applications.

– Ambiguous storage market position: Uncertainty persists regarding storage’s classification as a novel market participant or alignment with existing categories. Additionally, dispatch protocols for non-hydraulic storage units remain undefined.

Bankability: A Key to Project Development

Bankability—a project’s capacity to attract financing based on economic and technical viability—remains a critical consideration for energy storage initiatives in Latin America.

Despite declining technology costs, project bankability remains heavily contingent upon jurisdictional regulatory frameworks.

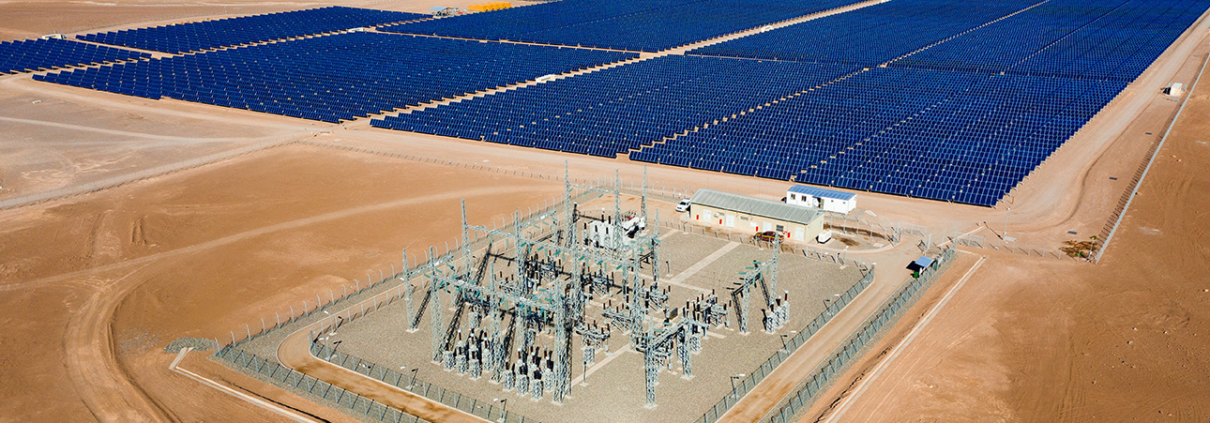

Chile exemplifies regional leadership by implementing legislation promoting electrical energy storage and electromobility. This framework enables storage systems to inject energy into the grid, operate under National Electric Coordinator agreements, and participate in energy and power transfers, valued according to grid marginal costs.

This regulatory environment facilitated Atlas Renewable Energy’s procurement of $289 million in financing for a 200 MW/800 MWh battery energy storage system (BESS) project in Chile’s desert region. Among Latin America’s largest storage installations, this initiative secured funding from premier international institutions, including BNP Paribas and Crédit Agricole, demonstrating global financiers’ appetite for projects with robust business models and supportive regulatory frameworks.

Subsequently, Atlas Renewable Energy executed a power purchase agreement (PPA) with COPEC (Compañía de Petróleos de Chile), ensuring clean, sustained electricity delivery over a 15-year term, leveraging storage to guarantee controlled energy distribution.

Following this, Atlas secured a BESS-integrated PPA with Chile’s state-owned mining corporation CODELCO, commencing energy delivery in 2026 for a 15-year duration.

Expanding its mining sector presence, Atlas signed another significant PPA with Grupo CAP to provide 450 GWh annually of clean energy to subsidiaries CMP and Aguas CAP. This third BESS-integrated project in the Atacama region brings Atlas’ total development portfolio to 475 MW of solar capacity paired with 616 MW of storage solutions.

Indeed, energy-intensive enterprises requiring continuous competitive power increasingly gravitate toward these PPAs, capturing surplus wind and/or solar generation for strategic dispatch, ensuring consistent, clean energy delivery to consumers.

The Latin American Experience

Chile’s sophisticated regulatory framework, which continues to evolve—as evidenced by Supreme Decree 70’s promulgation in June 2024—positions the nation as a regional leader in attracting energy storage investment.

National Energy Commission (CNE) data indicates Chile will achieve 1,113 MW of installed energy storage capacity by the end of 2024, with an average duration of approximately 3.88 hours. This capacity is projected to expand to 2,213 MW by the end of 2025, equivalent to 4.25 hours.

In Brazil, Latin America’s premier renewable energy market, the storage regulatory framework remains under development.

In 2023, the National Electric Energy Agency (Aneel) initiated public consultation regarding regulatory alternatives for storage integration. The agency proposed a three-cycle regulatory process:

– First cycle (2022–2023): Focusing on storage resource definition, service offering parameters, and regulatory barrier elimination.

– Second cycle (2023–2024): Addressing specific reversible hydroelectric plant considerations and storage economic viability analysis.

– Third cycle (2024–2025): Targeting complex elements, including service aggregator regulatory framework development and novel business model creation.

In September 2024, Brazil’s National System Operator (ONS) identified six regulatory priorities for the remainder of the year, including protocols governing energy storage, distributed generation, and ancillary services for National Interconnected System (SEN) management.

Colombia distinguishes itself among Latin America’s most advanced regulatory frameworks for storage. Resolution CREG 098 (2019) established comprehensive Battery Energy Storage Systems (BESS) integration mechanisms, including:

– Project execution: Delineating processes for selection, construction, and commissioning of storage projects, incorporating environmental criteria and connection requirements.

– Remuneration: Establishing operator compensation mechanisms based on economic offerings and costs across the project lifecycle—from construction to operation.

– Responsibilities: Delegating authority to the Mining and Energy Planning Unit (UPME) for agent selection and regulatory compliance oversight.

Building upon this foundation, the government has refined its framework, as exemplified by Resolution 101 023 (2022), defining service quality parameters for BESS, which was approved under Resolution CREG 098.

Mexico is another market demonstrating regulatory evolution. Despite specific project advancement, the jurisdiction faces substantial regulatory challenges requiring comprehensive technology integration resolution. In October 2024, Mexican authorities approved Administrative Provisions of General Character (DACG) governing the integration of energy storage systems into the National Electric System (SEN).

These provisions notably define various storage integration modalities:

1. SAE-CE (Power Plant Associated): Facilitates SAE integration with intermittent generation facilities, including solar or wind installations.

2. SAE-CC (Load Center Associated): Enables SAE integration with load centers, such as industrial or commercial complexes, independent of generation facilities.

3. SAE-AA (Isolated Supply Scheme) Incorporates SAE within power plants that primarily serve discrete consumer groups outside the national grid.

4. Unassociated SAE: Permits independent SAE operation, enabling direct energy injection into the National Transmission Grid (RNT) or General Distribution Networks (RGD).

Conclusion

Energy storage is indispensable in ensuring grid stability and facilitating renewable energy integration across Latin America.

As technological advancement accelerates and costs decline, storage systems increasingly present viable solutions. However, regulatory framework deficiencies continue to impede widespread adoption, ultimately determining project bankability.

Industry leaders such as Atlas Renewable Energy are demonstrating how storage projects can achieve feasibility, sustainability, and transformative impact within the regional energy landscape.

As battery economics continue to improve and regulatory frameworks mature, energy storage will increasingly assume a central role in Latin America’s energy transformation trajectory.

This article was created in partnership with Castleberry Media. At Castleberry Media, we are dedicated to environmental sustainability. By purchasing carbon certificates for tree planting, we actively combat deforestation and offset our CO₂ emissions threefold.

Share This Entry