10 Gigawatts. 18 Months. Latin America’s Window to Power the AI Era

An overlooked 10+ GW of grid-ready capacity, a significant cost advantage and a narrow window to reshape the global map of AI infrastructure.

By Lucas Salgado, Global Strategy Director and Head of Data Center & Powerland, Atlas Renewable Energy

The global race to build AI infrastructure is often framed as a contest between the United States, Europe and APAC. Developers in the United States face an interconnection queue of more than 2,600 GW [1], over twice the country’s entire installed generation, with median wait times approaching five years [2]. Europe has roughly 1,700 GW of renewable capacity stalled in grid connection processes [3], while APAC’s most attractive hubs are running out of headroom. Latin America, by contrast, may have the world’s most overlooked advantage: an immediately available, low-cost power base capable of hosting gigawatts of AI computing.

The premise of this article, and a central theme of the discussion at DCPI-LATAM, is that Latin America is not a secondary market waiting its turn. It is a substantial, underused power base with a real opportunity to capture near-term AI infrastructure demand. Whether the region serves only as a temporary bridge while other markets clear their queues, or establishes a lasting position as a hub for the digital economy, will depend on what happens over the next 12 to 18 months and on how effectively the obstacles described below are addressed.

A near-term power advantage

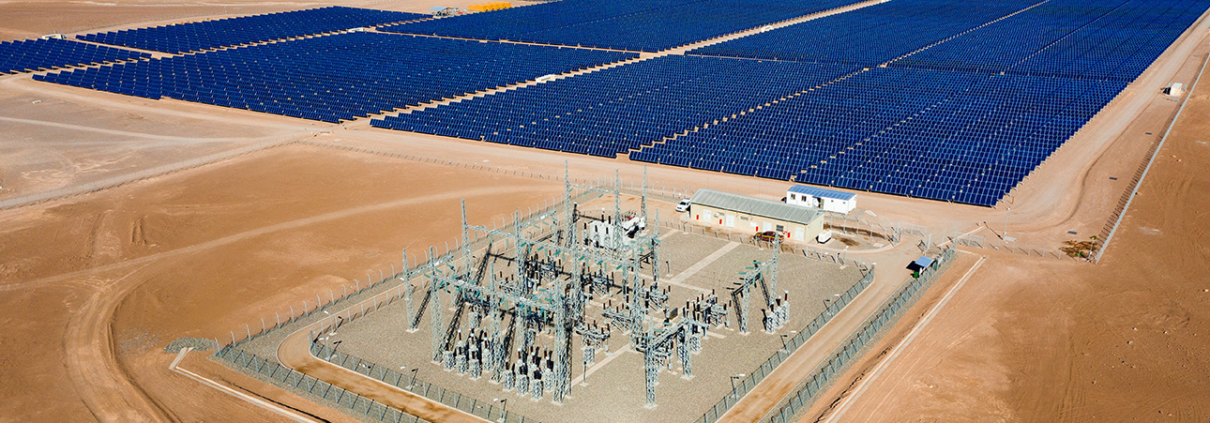

Latin America has more than 10 GW of grid-ready renewable capacity that could be made available to large loads over the next two to three years [A]. In Brazil and Chile alone, more than 1 GW is available at specific points of interconnection [A]. Curtailment in Brazil exceeded 20% of total solar and wind output in 2025, representing a loss of roughly USD 1.2 billion [4]. By 2029, the grid operator projects that up to 96% of curtailment will be driven by structural oversupply rather than operational constraints [5]. This is not a capacity problem. It is a demand problem.

The region’s power prices reflect this imbalance. All-in renewable PPA prices in Brazil, Chile and Mexico are below USD 0.06/kWh [A], well under half the cost of comparable contracts in many U.S. and European markets. Equipment lead times to Latin America run 30 to 50% faster than to comparable U.S. locations [A], and land availability is not a constraint. The physical and economic foundation is in place.

Why Latin America has not already captured a larger share

If the grid, the economics and the timeline all favor Latin America, why has the region not already captured a larger share of global AI infrastructure investment? The answer is not the grid, nor is it the underlying economics. The barriers are regulation, permitting, financing structures and execution risk. The central question is whether the region’s institutional machinery can move at the speed the industry now expects.

Two pending regulatory measures illustrate the problem in Brazil. The first is REDATA (Regime Especial de Tributação para o Setor de Datacenters), a proposed special tax regime that would suspend the federal taxes and import duties Brazil normally levies on servers, transformers and other high-value equipment. These charges can otherwise add double-digit percentages to a project’s capital budget.

The second concerns Article 21A of the rules governing Brazil’s Export Processing Zones (Zonas de Processamento de Exportação), which extend customs and tax relief to qualifying operations. Delay on either front reintroduces, through the tax code, much of the cost burden that Brazil’s competitive power prices would otherwise eliminate.

BESS deployment faces a related challenge. High import taxes continue to slow battery storage buildout in Brazil, even as storage becomes more central to firming renewable supply for large loads.

The obstacles extend beyond tax policy. In Chile, environmental licensing has frozen or cancelled high-profile projects. In Brazil, municipal-level approvals remain a recurring risk for hyperscalers evaluating sites. In Mexico, the interconnection process remains opaque on both cost and timing for grid reinforcements. Recent delays in system expansion and the energization of data center buildings in Querétaro have added further uncertainty.

Financing is another hurdle. Large-scale AI infrastructure requires long-tenor capital, and currency risk, political cycles and permitting uncertainty all affect how lenders and hyperscalers price that risk in Latin America relative to more established markets. Connectivity also has to keep pace. Without sufficient subsea cables, terrestrial backbones and fiber corridors, grid capacity alone will not be enough to close deals.

None of these problems are unusual for a fast-growing market, and none of them are unsolvable. However, they require deliberate and coordinated work. That includes clear regulation guaranteeing power capacity to large loads, sustained investment in grid reinforcement, continuity of the policies that made renewables competitive in the first place, and better incentives, including tax relief, for BESS deployment.

Turning potential into projects

Closing these gaps depends on utilities, regulators, hyperscalers, developers and financiers working from the same picture of what is achievable and on what timeline. This is precisely the value of forums like DCPI-LATAM, the 1st LATAM Data Center Power & Infrastructure Summit taking place July 14–15 in Rio de Janeiro.

Bringing these groups into the same room, rather than negotiating market by market and project by project, is one of the most direct ways to convert this narrow window into real, contracted capacity.

A bridge or a lasting digital hub?

Taken together, Latin America offers a combination that is genuinely difficult to find elsewhere: abundant land, a power grid with real near-term headroom, some of the most competitive renewable energy anywhere, and a deep pool of STEM talent across countries that have built world-class engineering, operations and digital capabilities over the last two decades.

Used well, this window could allow the region to host gigawatt-scale AI deployments at a pace few other markets can match. The near-term opportunity is to serve as a bridge, providing a place where hyperscalers and AI companies can land capacity while their U.S., European and APAC pipelines slowly clear. This opportunity is emerging against a global AI data center demand forecast that is expected to grow 3.5 times by 2030, reaching 156 GW worldwide [6].

The longer-term opportunity is structural. Latin America has the natural and institutional ingredients to become a lasting hub of the digital economy, provided its regulators, financiers and infrastructure developers close the execution gap at the same pace the market is moving.

From opportunity to execution

On Tuesday, July 14, Lucas Salgado will join Equinix, Ascenty and Alvarez & Marsal on the opening panel at DCPI-LATAM, “Break the Energy Bottleneck: Scaling Generation from Megawatts to Gigawatts.”

Three questions will frame the discussion. How are energy producers and utilities planning the jump from 20 MW data centers to 500 MW-plus AI campuses? What self-generation and behind-the-meter strategies are operators choosing while transmission catches up? How do energy, fiber and connectivity requirements vary across Latin American markets, and what does that mean for where infrastructure ultimately gets built?

The central premise is clear: the region already has the energy. What it needs now is regulatory clarity, coordinated infrastructure investment and financing, and the speed of execution required to convert that energy into operating gigawatts before the window narrows further.

The capacity is there and the economics are compelling, but capturing the opportunity will require sustained coordination among regulators, utilities, developers and investors. The opportunity is real. The question is whether Latin America can move quickly enough to capture it before the window closes.

Sources & References

Published sources:

[1] Lawrence Berkeley National Laboratory, “Queued Up”: U.S. interconnection queue data through 2024 (2,600 GW of generation and storage seeking grid connection): https://emp.lbl.gov/queues

[2] Novogradac, “Resolving the Interconnection Queue Bottleneck…” (January 2026): PJM 2025 projects averaging 8 years in queue; median U.S. wait time approaching 5 years: https://www.novoco.com/notes-from-novogradac/resolving-the-interconnection-queue-bottleneck…

[3] Enki AI / industry market intelligence (April 2026): Approximately 1,700 GW of renewable energy projects delayed in European grid connection processes as of 2025: https://enkiai.com/ai-market-intelligence/grid-interconnection-delays-2026…

[4] PV Magazine / Volt Robotics Annual Curtailment Report (February 2026): Brazil curtailed 20.6% of solar and wind output in 2025; estimated loss of BRL 6.5 billion (USD 1.2 billion); average generation cuts of 4,021 MW: https://www.pv-magazine.com/2026/02/02/brazil-curtails-20-of-solar-and-wind-output…

[5] U.S. Department of Commerce / International Trade Administration, “Brazil Energy Curtailment” (January 2026): ONS projection that by 2029 up to 96% of curtailment will be driven by structural supply-demand imbalance: https://www.trade.gov/market-intelligence/brazil-energy-curtailment

[6] McKinsey & Company / Camus Energy reference: Global AI data center demand forecast to grow 3.5 times from 2025 to 2030, reaching 156 GW worldwide: https://www.camus.energy/blog/why-does-it-take-so-long-to-connect-a-data-center-to-the-grid

Atlas analysis & internal market intelligence:

[A] Atlas Renewable Energy internal market analysis, based on its operational portfolio, project pipeline across Brazil, Chile, Mexico and Colombia, and active commercial engagement with hyperscaler clients. The analysis includes: (i) more than 10 GW of grid-ready capacity available across Latin American markets over the next two to three years; (ii) more than 1 GW available at specific points of interconnection in Brazil and Chile; (iii) DC and HV equipment lead times to Latin America running 30–50% faster than to comparable U.S. locations; and (iv) all-in renewable PPA prices below USD 0.06/kWh in Brazil, Chile and Mexico.

Event reference:

[E] 1st LATAM Data Center Power & Infrastructure Summit. Agenda, July 14–15, 2026, Rio de Janeiro. Panel: “Break the Energy Bottleneck: Scaling Generation from Megawatts to Gigawatts”: https://newenergyevents.com/dcpi-latam/agenda

Lucas Salgado

Lucas Salgado is Global Strategy Director and Head of the Data Center & Powerland unit at Atlas Renewable Energy, BlackRock-GIP’s renewable energy and infrastructure platform in Latin America. He will speak on the opening panel of DCPI-LATAM on July 14 in Rio de Janeiro.

Share This Entry